|

| Dees Illustration |

Eric Blair

Activist Post

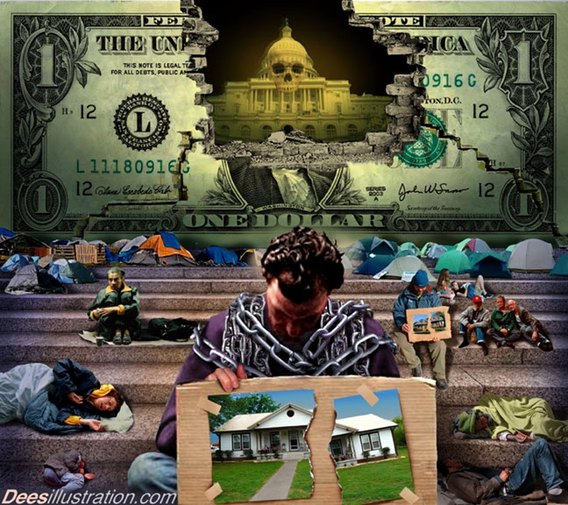

President Obama proposed raising the national minimum wage to $9/hour during his State of the Union address drawing cheers from the left.

Unfortunately they have little understanding of economics. Forced minimum wages will destroy or offshore many more jobs in America.

The left doesn’t seem to understand that the state can’t raise the standard of living for a populace through wage legislation. Additionally, raising the minimum wage doesn’t address the root of the problem of why the standard of living is declining in the first place.

Those who genuinely care about social justice look for someone to blame for the declining standard of living; greedy business men, illegal immigrants for driving down wages, politicians who oppose minimum wage laws and so on. None of these are the real enemy.

As G. Edward Griffin wrote in The Creature From Jekyll Island;

The American people have no idea they are paying the bill. They know that someone is stealing their hubcaps, but they think it is the greedy businessman who raises prices or the selfish laborer who demands higher wages or the unworthy farmer who demands too much for his crop or the wealthy foreigner who bids up our prices. They do not realize that these groups also are victimized by a monetary system which is constantly being eroded in value by and through the Federal Reserve System. (pg. 33).

Our fractional reserve fiat monetary system has inflation built into it, causing higher prices for all goods and services. When wages aren’t increased to match the higher cost of living, workers feel the pinch and demand that lawmakers do something.

However, the answer to social justice isn’t raising wages through legislation, because that will in turn just raise the cost of living even more because businesses will have to pass those costs on to customers. Not because they’re greedy, but because they have to survive.

For those who really want social justice, the solution is addressing a blood-sucking monetary system and restore sound money. Until then, all actions will be counterproductive to their good intentions.

Here’s a short video that clearly explains the consequences of raising the minimum wage in global economy:

Read other articles by Eric Blair Here

Using common sense, if raising the minimum wage will not kill jobs then why not raise the minimum wage to $25.00 or $50.00 or $100.00 per hour? Of course there are consequences that either are reflected in job elimination or increased prices. Virtually never are the OWNERS of corporations willing reduce profits. If wage levels were not a factor there would be no reason for ANY company to exit production in the United States and move production to foreign lands with significantly less labor costs. Also, there is the impact on pricing levels, as any increases in the cost of production or service always results in pricing increases.

If this were not the case, then no companies would be compelled to seek other more cost-efficient means of production or to move production to foreign countries whose workers are paid far less than Americans. Increasingly, companies are seeking more efficient and less long term costs that non-human technology can deliver to reduce their operating costs, provide higher build quality, automate service, and maximize profits for their OWNERS. As is virtually always the case, the OWNERS of companies do not want to reduce profits.

What the proponents of raising the minimum wage fundamentally are addressing is that low-paid American workers need to earn more income.

We need to begin focusing on the means for people to earn more income, not dependent on earnings from jobs, which are being destroyed with tectonic shifts in the technologies of production. We need to implement financial mechanisms to finance future economic growth and simultaneously create new capital asset owners. This can be accomplished with monetary reform and using insured, interest-free capital credit (without the requirement of past savings), repayable out of the future earnings in the investments in our economy’s growth.

But how, you ask, can such an OWNERSHIP CREATION solution be implemented?

We can and should do more to create universal capital ownership not only for workers of corporations but ALL citizens. What I believe is crucial to solving economic inequality and building a future economy that can support general affluence for EVERY citizen is to address concentrated capital ownership, the fundamental cause of economic inequality. The obvious solution is to de-concentrate capital ownership by ensuring that all future wealth-creating, income-producing capital asset formation will be financed using insured, interest-free capital credit, repayable out of the future earnings of the investments, creating ownership participation by EVERY child, woman, man. This should be about investment in real productive capital growth, not speculation as with the stock exchanges. But the problem is, whether with his call for tax credits and health savings accounts, that the vast majority of Americans have no savings, or at best extremely limited savings, insufficient to be meaningful as increasingly Americans are living week to week, month to month, and deeply in consumer debt. So there is no feasible way that past savings can continue to be a requirement for investment if we are to simultaneously create new capital owners with the productive growth of the economy. The current economic investment system is structured based on the requirement of past savings used directly or as security for capital credit loans. But past savings are not necessary as viable capital formation projects pay for themselves. This is the logic of corporate finance.

Capital acquisition takes place on the logic of self-financing and asset-backed credit for productive uses. People invest in capital ownership on the basis that the investment will pay for itself. The basis for the commitment of loan guarantees is the fact that nobody who knows what he or she is doing buys a physical capital asset or an interest in one unless he or she is first assured, on the basis of the best advice one can get, that the asset in operation will pay for itself within a reasonable period of time––5 to 7 or, in a worst case scenario, 10 years (given the current depressive state of the economy). And after it pays for itself within a reasonable capital cost recovery period, it is expected to go on producing income indefinitely with proper maintenance and with restoration in the technical sense through research and development.

Still, there is at least a theoretical chance, and sometimes a very real chance, that the investment might not pay for itself, or it might not pay for itself in the projected time period. So, there is a business risk. This can be solved using private capital credit insurance or a government reinsurance agency (ala the Federal Housing Administration concept). On a larger scale, the path to solve the security issue, that is, the risk can be absorbed by capital credit insurance or commercial risk insurance. Thus, in order to achieve national economic democracy, we need a way to handle risk management in finance by broadly insuring the risks. Such capital credit insurance would substitute for the security demanded by lenders to cover the risk of non-payment, thus enabling the poor and others with no or few assets (the 99 percenters) to overcome the collateralization barrier that excludes the non-halves from access to productive capital.

One feasible way is to lift ownership-concentrating Federal Reserve System credit barriers and other institutional barriers that have historically separated owners from non-owners and link tax and monetary reforms to the goal of expanded capital ownership. This can be done under the existing legal powers of each of the 12 Federal Reserve regional banks, and will not add to the already unsustainable debt of the Federal Government or raise taxes on ordinary taxpayers. We need to free the system of dependency on Wall Street and the accumulated savings and money power of the rich and super-rich who control Wall Street. The Federal Reserve System has stifled the growth of America’s productive capacity through its monetary policy by monetizing public-sector growth and mounting Federal deficits and “Wall Street” bailouts; by favoring speculation over investment; by shortchanging the capital credit needs of entrepreneurs, inventors, farmers, and workers; by increasing the dependency of with usurious consumer credit; and by perpetuating unjust capital credit and ownership barriers between rich Americans and those without savings. The Federal Reserve Bank should be used to provide interest-free capital credit (including only transaction and risk premiums) and monetize each capital formation transaction, determined by the same expertise that determines it today––management and banks––that each transaction is viably feasible so that there is virtually no risk in the Federal Reserve. The first layer of risk would be taken by the commercial credit insurers, backed by a new government corporation, the Capital Diffusion Reinsurance Corporation, through which the loans could be guaranteed. This entity would fulfill the government’s responsibility for the health and prosperity of the American economy.

The Federal Reserve Board is already empowered under Section 13 of the Federal Reserve Act to reform monetary policy to discourage non-productive uses of credit, to encourage accelerated rates of private sector growth, and to promote widespread individual access to productive credit as a fundamental right of citizenship. The Federal Reserve Board needs to re-activate its discount mechanism to encourage private sector growth linked to expanded capital ownership opportunities for all Americans.

Until we address concentrated capital ownership and implement solutions to simultaneously broaden capital ownership by creating new capital owners with the growth of the productive economy, money power will reside in the hands of politicians and bankers, not in the hands of the citizens. That is why to reform the system leaders and advocates for economic justice must focus on money, how it should be created and measured, how it should be controlled and why a more realistic and just money system is the key to universal and equal citizen access to future ownership opportunities as a fundamental human right. Then prosperity and economic democracy can serve as the basis for effective and non-corruptible political democracy, an ecologically sustainable environment, and global peace through justice.