By Daisy Luther

By Daisy Luther

After Silicon Valley Bank had its deposits seized by the FDIC, on a Friday, as predicted, there’s a sense of unease across the country. Depositors have been unable to access their funds, and we’re all wondering, “Am I next?” Many of us are quickly making a transition to physical investments we can hold in our hands because the future of banking is incredibly concerning.

On Sunday night, a second bank was closed by regulators and its deposits have also been put in control of the FDIC. Signature Bank out of New York was shut down to “protect consumers and the financial system,” according to a joint statement released by the U.S. Treasury Department, the Federal Reserve, and the Federal Deposit Insurance Corporation.

According to that statement:

Depositors of the Silicon Valley Bank will have access to all of their money – following the bank’s failure on Friday – at no loss to American taxpayers…

…”Today we are taking decisive actions to protect the U.S. economy by strengthening public confidence in our banking system,” the joint statement read. “This step will ensure that the U.S. banking system continues to perform its vital roles of protecting deposits and providing access to credit to households and businesses in a manner that promotes strong and sustainable economic growth.”

The statement said Treasury Secretary Janet L. Yellen had approved actions enabling the FDIC to complete its resolution of SVB “in a manner that fully protects depositors.”

Depositors will have access to all of their money starting Monday, March 13. The taxpayer will bear no losses associated with the resolution of SVB.

Notably, the regulators’ statement also announced the shutdown of New York-based Signature Bank.

“We are also announcing a similar systemic risk exception for Signature Bank, New York, New York, which was closed today by its state chartering authority,” the joint statement read.

So that’s two down.

And while they’re saying that isn’t a bail-out, it sure sounds like a bail-out. More on that shortly.

What we could be facing is anything from “watch and wait” to bank runs to a market collapse. I’ll update throughout the day.

Beware the banking information blackout

I started writing this article on Sunday afternoon, and I’m finishing it at 3 am US time and will update today, Monday, March 14th, as the situation unfolds.

Congress has already talked about censoring any “bad actors” who dare to talk about this banking collapse.

Just got off of a zoom meeting with Fed, Treasury, FDIC, House, and Senate.

A Democrat Senator essentially asked whether there was a program in place to censor information on social media that could lead to a run on the banks.

— Thomas Massie (@RepThomasMassie) March 13, 2023

Please watch your email (sign up here) or check back directly to get updates.

A number of sources I cited in my Sunday research have already been removed. If you click and face broken links, that’s why. I took screenshots of some things but not of others. (Unfortunately – silly me.) This is also why you may see sources here that I don’t generally use.

I’ll provide the best information I can during this crisis and my best assessment of what’s going on.

Who’s next?

You’re probably wondering who’s next. What banks will be targeted by the FDIC for shutdown, and is it one that YOU use?

While it’s impossible to predict – Signature Bank was not included in the warning lists that I’ve found – here’s what we know about banks with numbers that look similar to SVB, as well as some really interesting information about the collapse of Silicon Valley Bank that you may not have heard yet.

The Ultimate Guide to Frugal Living: Save Money, Plan Ahead, Pay Off Debt & Live Well by Daisy Luther

The Ultimate Guide to Frugal Living: Save Money, Plan Ahead, Pay Off Debt & Live Well by Daisy Luther

These banks are concerning some experts.

While it’s impossible to say which banks are next to fall, there are some institutions that are sitting in precarious situations. According to Morningstar.com, these banks “raised similar red margin flags to those of SVB.” They show negative accumulated other comprehensive income “as a percentage of total equity capital.” (NOTE: Since I wrote this article last night, the article on Morningstar.com has been taken down. Hmmm….some of that censorship that Congress was talking about?)

- Customers Bancorp Inc. of West Reading, PA

- First Republic Bank of San Francisco, CA

- Sandy Spring Bancorp Inc. of Olney, MD

- New York Community Bancorp Inc. of Hicksville, NY

- First Foundation Inc. of Dallas, TX

- Ally Financial Inc of Detroit, MI

- Dime Community Bancshares Inc. of Hauppauge, NY

- Pacific Premier Bancorp Inc. of Irvine, CA

- Prosperity Bancshare Inc. of Houston, TX

- Columbia Financial, Inc. of Fair Lawn, NJ

But these aren’t the only organizations at risk as per Morningstar. These had some of “the highest ratios of negative AOCI to total equity capital less AOCI.”

- Comerica Inc. of Dallas, TX

- Zions Bancorporation of Salt Lake City, UT

- Popular Inc. of San Juan, PR

- KeyCorp of Cleveland, OH

- Community Bank System Inc. of DeWitt, NY

- Commerce Bancshares Inc. of Kansas City, MO

- Cullen/Frost Bankers Inc. of San Antonio, TX

- First Financial Bankshares Inc. of Abilene, TX

- Eastern Bankshares Inc. of Boston MA

- Heartland Financial USA Inc. of Denver, CO

- First Bancorp FBNC of Southern Pines, N.C.

- Silvergate Capital Corp. of La Jolla, CA

- Bank of Hawaii Corp. of Honolulu, HI

- Synovus Financial Corp. of Columbus, GA

Some reports say that Silvergate, a crypto-focused bank, has already gone under.

Stuff you couldn’t make up

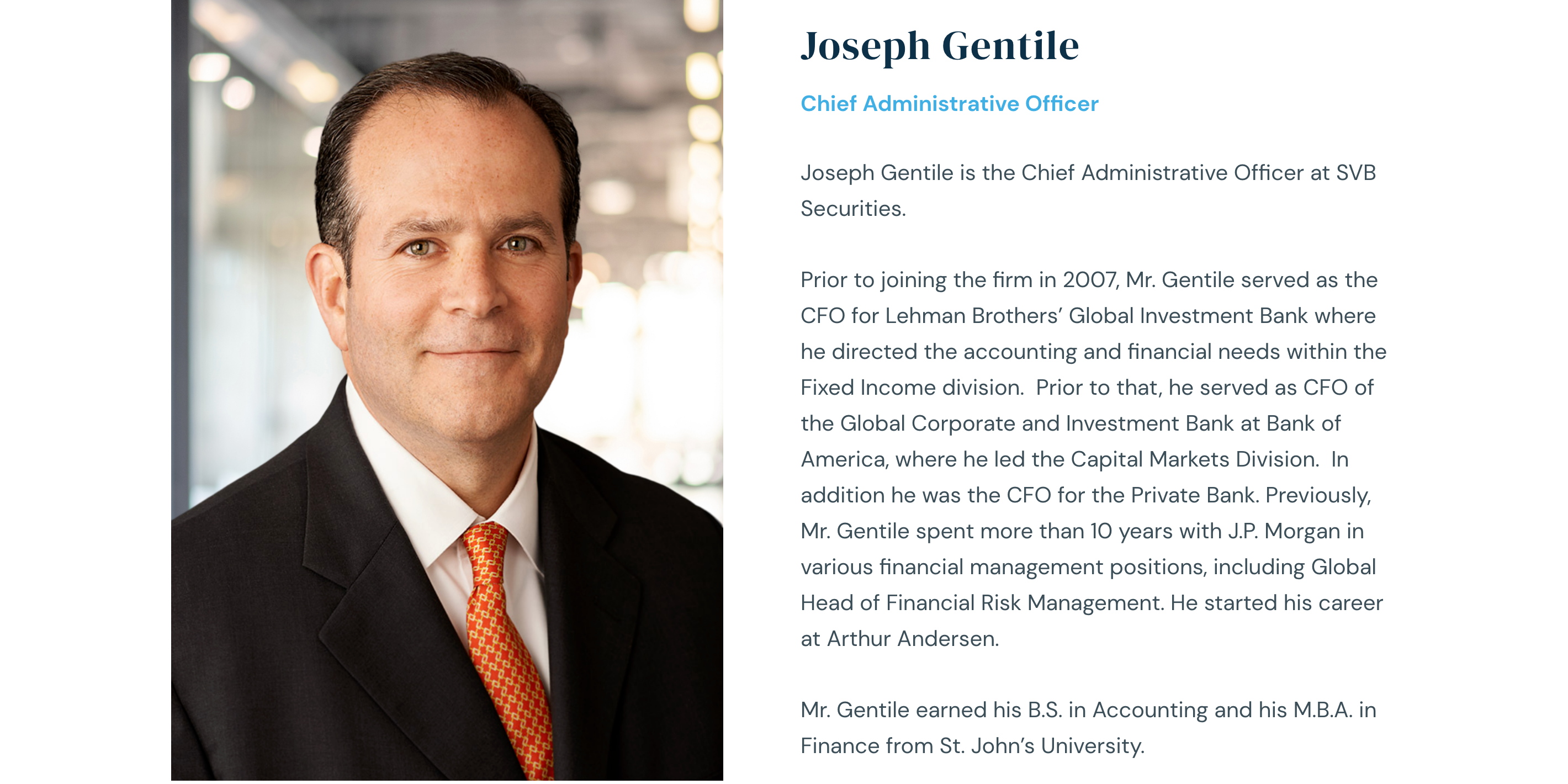

It’s extremely interesting to note one specific fact about Joseph Gentile, the CAO of SVB. Gentile seems to have a history of being at the helm of ships that sink in a very dramatic fashion. In fact, his job before SVB was at…

…

Lehman Brothers.

Yes. That Lehman Brothers.

Prior to joining the firm in 2007, Mr. Gentile served as the CFO for Lehman Brothers’ Global Investment Bank where he directed the accounting and financial needs within the Fixed Income division.

It’s like one of those “crisis actors” that certain factions swear show up at every horrible mass-casualty event.

Except, this one is absolutely and irrefutable true.

Is Gentile simply the worst banker on the planet? The victim of horribly bad karma? Or is there something more at play here? An article on Breitbart goes further into the background of Mr. Gentile.

SVB employees got their bonuses hours before things went south.

Anyway, mere hours before the FDIC took over, SVB employees were paid bonuses.

The Santa Clara, California-based bank has historically paid employee bonuses on the second Friday of March, said the people, who declined to be identified speaking about the awards. The payments were for work done in 2022 and had been in process days before the bank’s collapse, the sources said.

This year, bonus day happened to fall on SVB’s final day of independence. The institution, in the throes of a bank run triggered by panicked venture capital investors and startup founders, was seized by the Federal Deposit Insurance Corporation (FDIC) around midday Friday…

…The size of the payouts couldn’t be determined, but SVB bonuses range from about $12,000 for associates to $140,000 for managing directors, according to Glassdoor.com.

I’m sure that all of this was mere coincidence. Right?

A few years ago, SVB lobbied Congress and won.

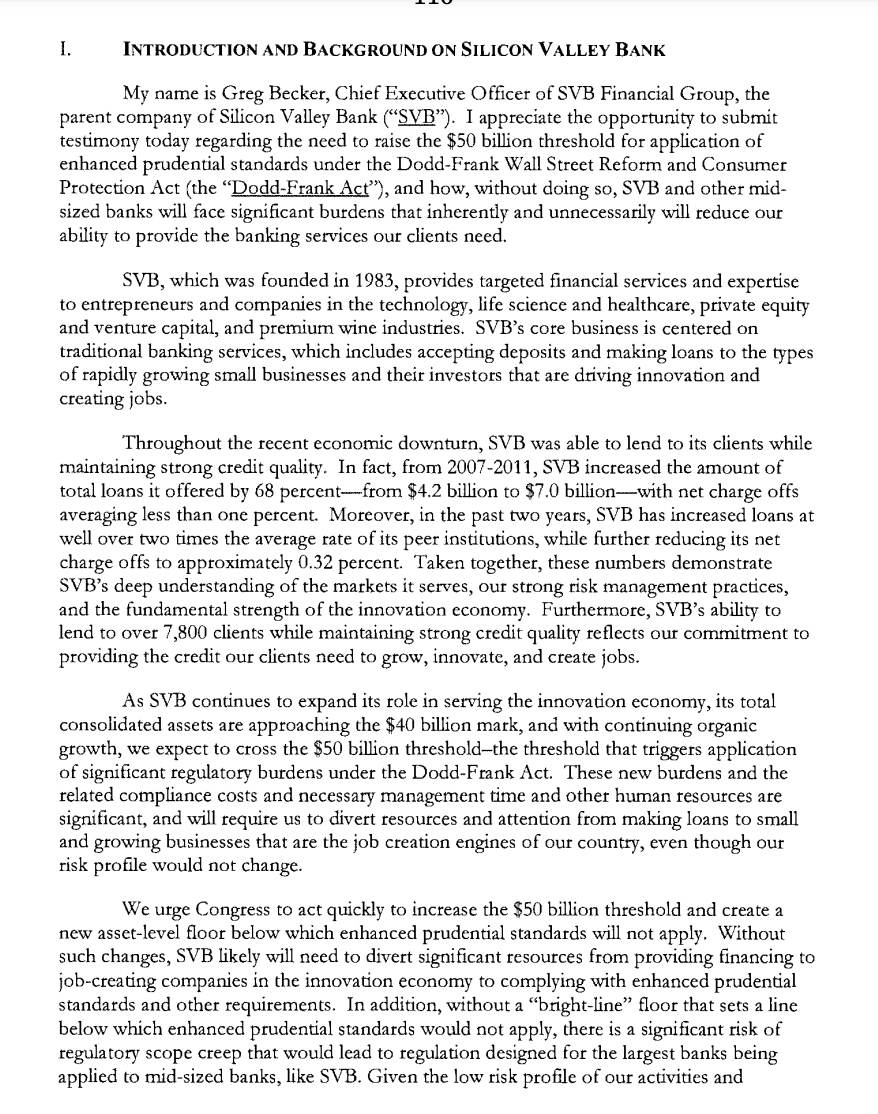

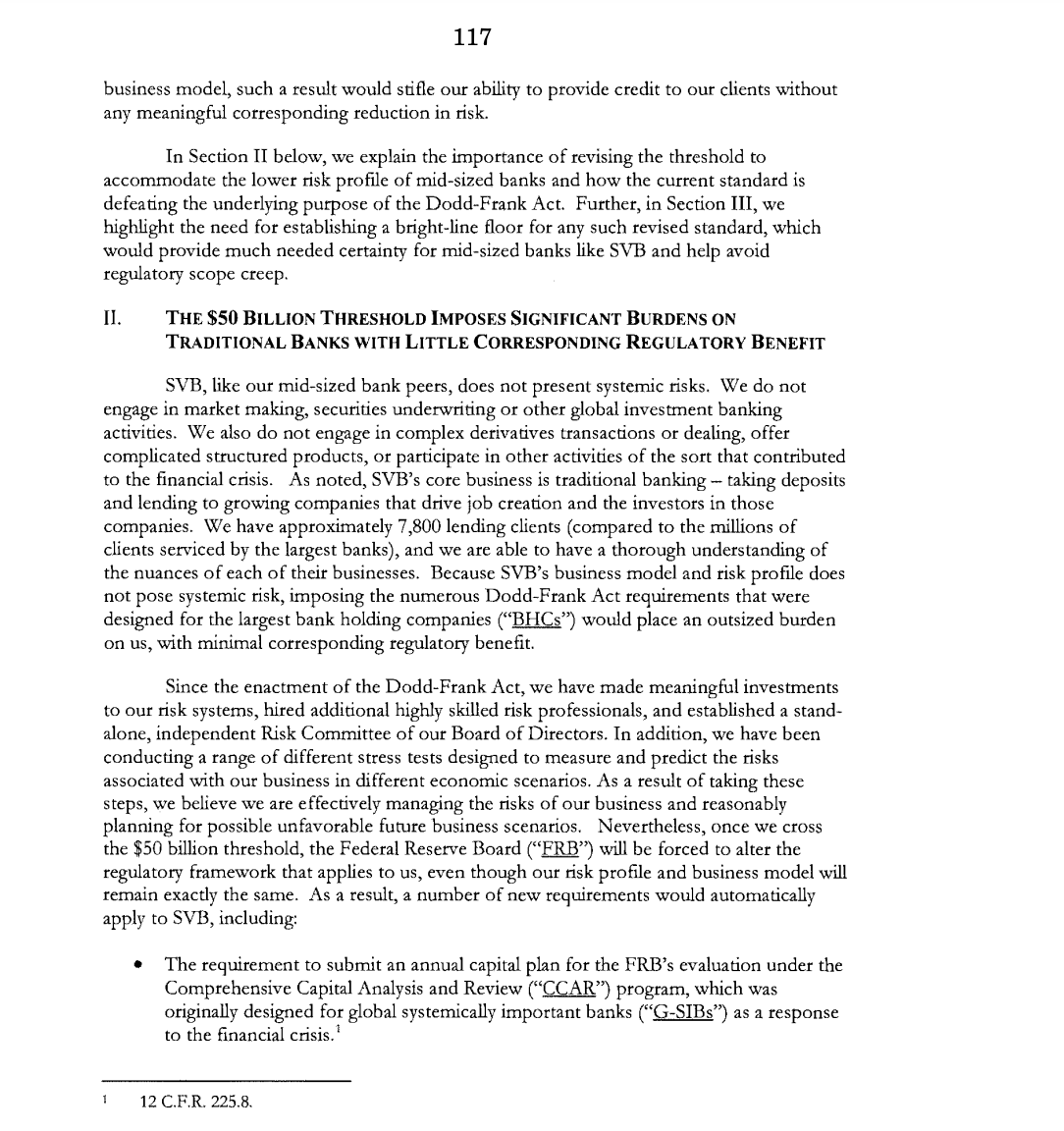

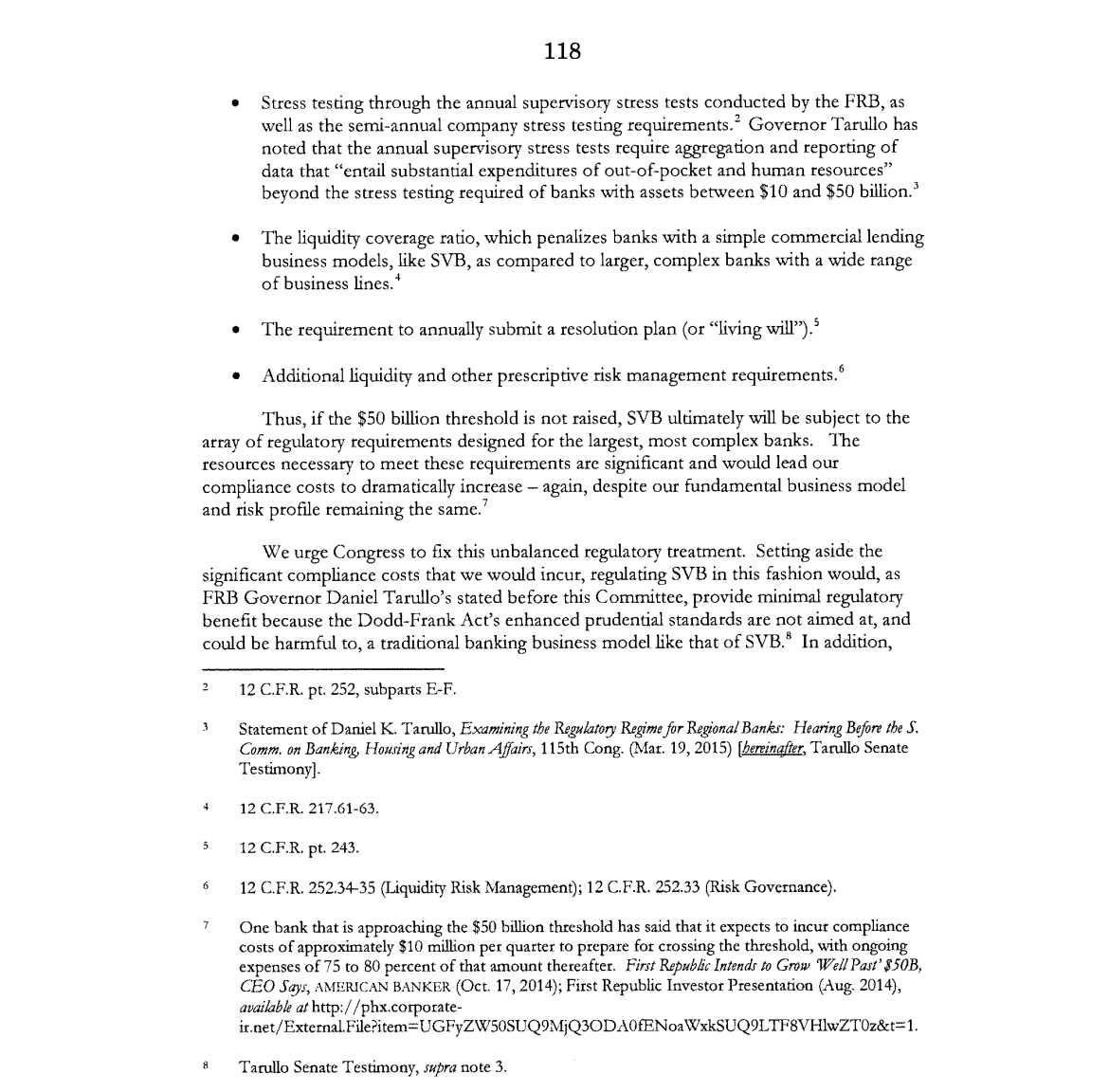

This story of risk started years ago. It’s not just a recent thing. Back in 2018 the CEO of SVB, Greg Becker, lobbied Congress to have the Dodd-Frank provisions on regional lenders relaxed. And he won.

In 2015, SVB Chief Executive Officer Greg Becker urged the government to increase the threshold, arguing it would otherwise lead to higher costs for customers and “stifle our ability to provide credit to our clients.” With a core business of traditional banking — taking deposits and lending to growing companies — SVB doesn’t pose systemic risks, he said.

Easiest way to get your first Bitcoin (Ad)

On page 215 of this document from the Senate Committee on Banking, Housing, and Urban Affairs, you can read Becker’s testimony. I’ve taken screenshots.

Make of this what you will.

SVB is affecting everyday people like you and me.

Incidentally, some people are trying to blow off the significance of the SVB failure, since it’s a higher-risk bank heavily involved in venture capital and start-ups. They feel that such a bank isn’t going to affect the everyday person.

Tell that to the Etsy sellers who’ve had their Friday payment delayed by the closure. I’m not sure how many people this affects, but I do know that Etsy is a platform that has allowed many people a way to earn a living in this crazy economy. I personally know several moms who’ve been able to stay home with their children due to the money they make from their Etsy business, and I also know people who do this full-time for a living.

Here’s what we know, from ESeller365.

“As you may have seen, we recently experienced a delay in our ability to issue payments to some of our sellers. This was related to the rapid and unexpected collapse of Silicon Valley Bank.

“We apologize for any inconvenience this has caused. Our teams have been working around the clock to implement a solution and ensure sellers are paid within the next few business days via our other payment partners.

“We are committed to helping you run your business — and providing a reliable experience is a critical part of that commitment. Please know our teams are working tirelessly to minimize future disruptions and continue to serve you as best we can.”

While there’s no prediction in that email when sellers will be paid, some vendors have stated that the new date showing up in their dashboard is March 13.

ESeller365 says that Etsy may not even be directly banking with SVB.

It’s also very possible Etsy didn’t even have its funds directly with SVB. But instead, one of its payment partners did, which could’ve caused this disruption as well.

That should certainly demonstrate the kind of ripple effects the closure of one bank, a relatively regional bank that is ranked in size in America, can have. As someone who is also reliant on my online business, I sincerely hope that these sellers are paid quickly and can get back to business as usual.

Here are some of the businesses that use(d) SVB

ZeroHedge provided a list of a number of businesses that had well over the insured $250K on deposit at SVB and could be affected. If they are, it could result in massive numbers of employees being laid off, vendors not getting paid, and other catastrophic ripples through the economy. (Visit ZH’s article at the previous link to get the details on each of these – many of the businesses listed have added statements.)

- USDC – Crypto Stablecoin run by Circle

- ROKU

- BLOCKFI

- RBLX – Roblox

- DNA – Gingko Bioworks

- RKLB – RocketLab USA

- LC – Lending Club

- PAYO – Payoneer

- PTGX – Protagonist Therapeutics

- ACHR – Archer Aviation

- COHU –

- IGMS – IMG Biosciences

- RYTM – Rhythm Pharmaceuticals

- SYRS – Syros Pharmaceuticals

- EYPT – EyePoint Pharmaceuticals

- ATRA – Atara Biotherapeutics

- ISEE – Iveric Bio

- VERA – Vera Therapeutics

- XFOR – X4 Pharmaceuticals

- CTMX – CytomX Therapeutics

- AXSM – Axsome Therapeutics

- WVE – Wave Life Science

- JNPR – Juniper Networks

- QS – QuantumScape

Perhaps if SVB had been less worried about their ESG policies and more concerned about their stewardship of people’s money, folks would not be facing the current predicament.

We sincerely hope these businesses will be able to recover from the closure without difficulty.

Billionaire warns of meltdown if there’s no bailout

Bill Ackman, the billionaire CEO of Pershing Square Capital Management, is adamant that if the government doesn’t bail out SVB, further disaster is imminent.

He posted on Twitter. (Spacing is mine for clarity)

The gov’t has about 48 hours to fix a-soon-to-be-irreversible mistake. By allowing @SVB_Financial to fail without protecting all depositors, the world has woken up to what an uninsured deposit is — an unsecured illiquid claim on a failed bank.

Absent @jpmorgan @citi or @BankofAmerica acquiring SVB before the open on Monday, a prospect I believe to be unlikely, or the gov’t guaranteeing all of SVB’s deposits, the giant sucking sound you will hear will be the withdrawal of substantially all uninsured deposits from all but the ‘systemically important banks’ (SIBs).

These funds will be transferred to the SIBs, US Treasury (UST) money market funds, and short-term UST. There is already pressure to transfer cash to short-term UST and UST money market accounts due to the substantially higher yields available on risk-free UST vs. bank deposits. These withdrawals will drain liquidity from community, regional and other banks and begin the destruction of these important institutions. The increased demand for short-term UST will drive short rates lower complicating the @federalreserve’s efforts to raise rates to slow the economy. Already thousands of the fastest growing, most innovative venture-backed companies in the U.S. will begin to fail to make payroll next week.

Had the gov’t stepped in on Friday to guarantee SVB’s deposits (in exchange for penny warrants which would have wiped out the substantial majority of its equity value), this could have been avoided, and SVB’s 40-year franchise value could have been preserved and transferred to a new owner in exchange for an equity injection. We would have been open to participating. This approach would have minimized the risk of any gov’t losses, and created the potential for substantial profits from the rescue.

Instead, I think it is now unlikely any buyer will emerge to acquire the failed bank. The gov’t’s approach has guaranteed that more risk will be concentrated in the SIBs at the expense of other banks, which itself creates more systemic risk.

For those who make the case that depositors be damned as it would create a moral hazard to save them, consider the feasibility of a world where each depositor must do their own credit assessment of the bank they choose to bank with. I am a pretty sophisticated financial analyst, and I find most banks to be a black box despite the 1,000s of pages of @SECGov filings available on each bank.

SVB’s senior management made a basic mistake. They invested short-term deposits in longer-term, fixed-rate assets. Thereafter short-term rates went up and a bank run ensued. Senior management screwed up and they should lose their jobs.

The @FDICgov and OCC also screwed up. It is their job to monitor our banking system for risk and SVB should have been high on their watch list with more than $200B of assets and $170B of deposits from business borrowers in effectively the same industry.

The FDIC’s and OCC’s failure to do their jobs should not be allowed to cause the destruction of 1,000s of our nation’s highest potential and highest growth businesses (and the resulting losses of 10s of 1,000s of jobs for some of our most talented younger generation) while also permanently impairing our community and regional banks’ access to low-cost deposits.

This administration is particularly opposed to concentrations of power. Ironically, its approach to SVB’s failure guarantees duopolistic banking risk concentration in a handful of SIBs. My back-of-the envelope review of SVB’s balance sheet suggests that even in a liquidation, depositors should eventually get back about 98% of their deposits, but eventually is too long when you have payroll to meet next week.

So even without assigning any franchise value to SVB, the cost of a gov’t guarantee of SVB deposits would be minimal. On the other hand, the unintended consequences of the gov’t’s failure to guarantee SVB deposits are vast and profound and need to be considered and addressed before Monday.

Otherwise, watch out below.

Today will certainly be interesting.

But there WON’T be a direct bail-out, according to Yellen

Despite Ackman’s pro-bailout argument, Janet Yellen, the Secretary of the Treasury, has stated that no bailout will be forthcoming for SVB, although they are working to help depositors.

Yellen, in an interview with CBS’ “Face the Nation,” provided few details on the government’s next steps. But she emphasized that the situation was much different from the financial crisis almost 15 years ago, which led to bank bailouts to protect the industry.

“We’re not going to do that again,” she said. “But we are concerned about depositors, and we’re focused on trying to meet their needs.”

With Wall Street rattled, Yellen tried to reassure Americans that there will be no domino effect after the collapse of Silicon Valley Bank.

“The American banking system is really safe and well capitalized,” she said. “It’s resilient.”

People with deposits at SVB will supposedly have access to all their money today, according to Yellen, and it won’t cost the American taxpayers any money.

However…

It sounds a lot like a bail-out. I remember 2008 and the bail-outs and they sounded a lot like this. Zero Hedge agrees:

The Fed also said that it is prepared to address any liquidity pressures that may arise, which in turn has just unveiled the first bailout acronym of the new crisis: the Bank Term Funding Program, or BTFP. Some more details:

The financing will be made available through the creation of a new Bank Term Funding Program (BTFP), offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.

The Fed explains that the Department of the Treasury will make available “up to $25 billion from the Exchange Stabilization Fund as a backstop for the BTFP.” And while the Federal Reserve – which was completely clueless about this banking crisis until Thursday – does not anticipate that it will be necessary to draw on these backstop funds, we anticipate that the final number of needed backstop liquidity be somewhere north of $2 trillion.

What is more notable is that the BTFP – or Buy The Fucking Pivot – facility, will pledge collateral at par, not at market value, thus giving banks credit for all those hundreds of billions in unrealized net losses, and allowing banks to “unlock liquidity” based on losses which the Fed and TSY now backstop!

Well, good. I’m sure everything’ll be just fine now. And it won’t cost taxpayers anything.

This crisis is not over. Here are my thoughts.

I can’t predict where this is going to go. I hope, sincerely, that the bleeding can be staunched and that this catastrophe doesn’t continue to spread through our banking system.

If it does, it would certainly be one way that CBDCs could be implemented with little backlash. Imagine Americans losing their money in a banking crisis, the money not being insured (as described here), and then being offered a way to recoup their account balances as long as they’re willing to take that wealth digitally.

I’ve said this every single time I’ve written about the economy lately. If you have savings you want to assure yourself you can keep, it’s time to consider holding physical gold and silver. I’m not talking about trying to do all your transactions with silver dimes. This is a strategy for money that isn’t currently being used and is just sitting there, presumably safe in the bank. I have advisors I strongly recommend, and they don’t charge a penny for consultations. Go here to learn more, or call them at 866-517-1257. Investing in precious metals is not just the domain of the wealthy. It’s for any of us who want to protect what we’ve worked hard to save.

We could be looking at a full-on stock market collapse today, or bank runs. This article discusses what to do in the event of a stock market crash.

What can you do if you’re worried about your money? Keep in mind that I’m not a financial advisor. This is based on what I’ve done myself.

- Withdraw cash – but know that this probably will be limited. Expect long lines, angry people, and empty ATM machines.

- Spend it – pay your bills early online or purchase essentials using your debit card. Fill up your vehicles and take care of the month’s expenses early so you can ride this out. (Hopefully things will have eased in a few days or weeks.)

- Switch it to precious metals. This is a strategy to use for the money you want to save and have hold its value.

Make the best decisions you can but realize that a great deal of this is out of your hands. You can only do what you can do.

And on that note…

Don’t panic.

Whatever you do, try not to panic.

This is something we’ve all prepared for and we knew it was coming at some point. It feels urgent right now because we’re watching it happen. But collapses have occurred before and will occur again. Even though this may be a more extreme scenario, know that we’re all in a similar boat and we’ll get through it.

Make your decisions calmly and rationally. Then go out and take a walk in nature, play a game with your kiddos, or watch a non-stressful movie. This is one of those big circle, little circle things that Selco talks about. There’s a limit to what you and I can do regarding the situation. Once that’s done, it’s out of our control. After that, all you can do is keep your cool and be ready to adapt.

What are your thoughts?

Is your bank one of the ones thought to be at risk? Have you been affected by this? What do you foresee happening next? What do you think about all the “coincidences” that led up to the fall of SVB?

Let’s talk about it in the comments section.

Source: The Organic Prepper

Daisy Luther is a coffee-swigging, adventure-seeking, globe-trotting blogger. She is the founder and publisher of three websites. 1) The Organic Prepper, which is about current events, preparedness, self-reliance, and the pursuit of liberty; 2) The Frugalite, a website with thrifty tips and solutions to help people get a handle on their personal finances without feeling deprived; and 3) PreppersDailyNews.com, an aggregate site where you can find links to all the most important news for those who wish to be prepared. Her work is widely republished across alternative media and she has appeared in many interviews.

Daisy is the best-selling author of 5 traditionally published books, 12 self-published books, and runs a small digital publishing company with PDF guides, printables, and courses at SelfRelianceand Survival.com You can find her on Facebook, Pinterest, Gab, MeWe, Parler, Instagram, and Twitter.

Become a Patron!

Or support us at SubscribeStar

Donate cryptocurrency HERE

Subscribe to Activist Post for truth, peace, and freedom news. Follow us on SoMee, Telegram, HIVE, Flote, Minds, MeWe, Twitter, Gab, What Really Happened and GETTR.

Provide, Protect and Profit from what’s coming! Get a free issue of Counter Markets today.

Be the first to comment on "A Second Bank CLOSED by FDIC: Who’s Next and What Should We Do?"